Treasury Secretary’s Expanded IRS Authority Draws Fresh Questions Amid Trump Tax Settlement Debate

Treasury Secretary’s Expanded IRS Authority Draws Fresh Questions Amid Trump Tax Settlement Debate

By

Alina Sinclair

Last updated:

June 4, 2026

First Published:

June 4, 2026

Photo: The Guardian

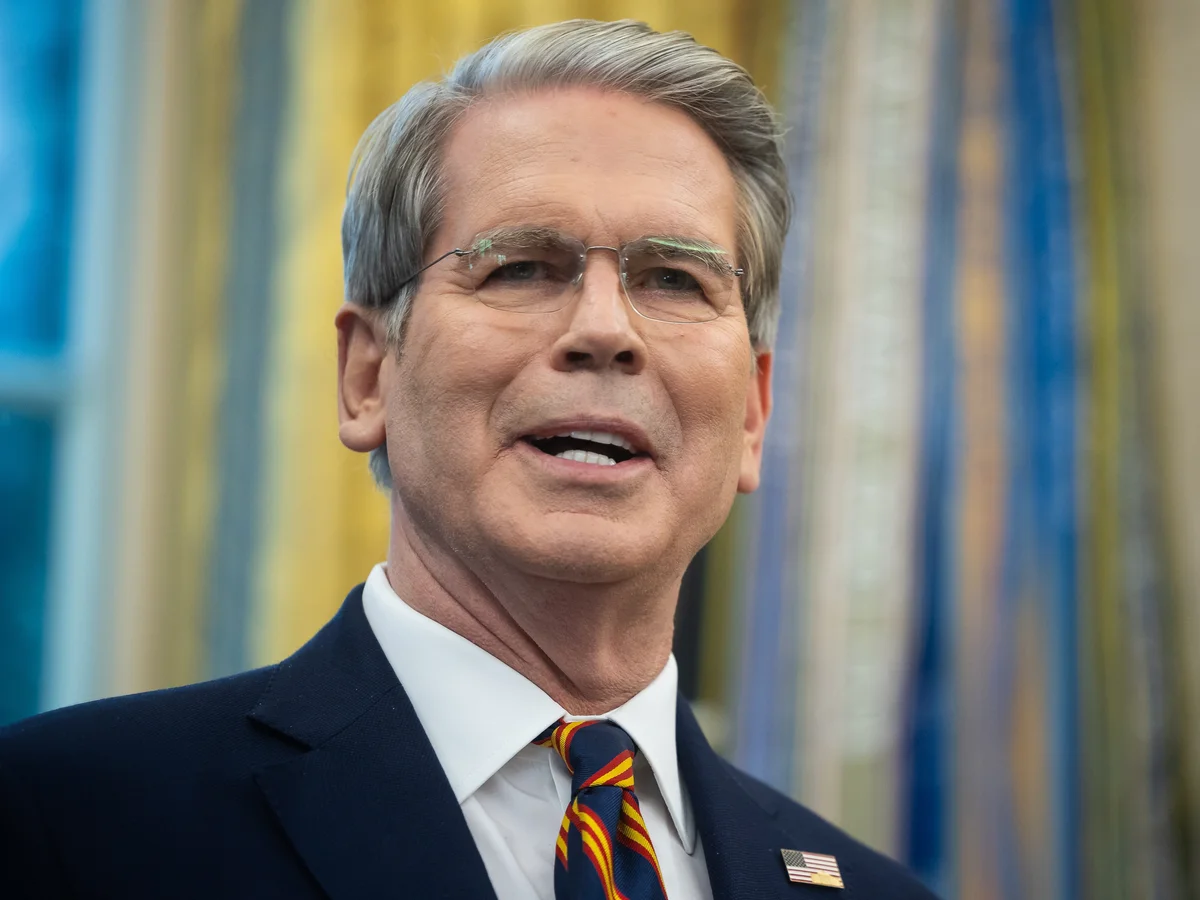

A contentious Senate hearing has placed renewed attention on the Internal Revenue Service's leadership structure and a controversial settlement involving President Donald Trump, as Treasury Secretary Scott Bessent acknowledged that he is currently carrying out many of the responsibilities typically assigned to the IRS commissioner.

The exchange has sparked broader questions about accountability, tax administration, taxpayer protections, and the federal government's handling of one of the most significant tax data leak cases in U.S. history.

At the center of the debate is an unusual leadership arrangement at the IRS and whether taxpayers affected by a massive tax information breach will receive treatment comparable to that provided under Trump's settlement agreement with the federal government.

A Leadership Gap at the IRS

During testimony before the Senate Finance Committee, Bessent clarified that while he is not officially serving as acting IRS commissioner, he is performing the duties normally associated with the position.

The distinction became a major point of discussion after lawmakers questioned who currently holds ultimate authority over key IRS decisions.

According to Treasury Department guidance issued earlier this year, Bessent's formal term as acting commissioner expired. However, because the commissioner position remains vacant, authority over certain functions has effectively shifted upward through the Treasury Department hierarchy.

As Treasury secretary, Bessent oversees the IRS, which operates as a bureau within the department and manages one of the largest administrative systems in the federal government.

The IRS processes hundreds of millions of tax returns annually, collects trillions of dollars in federal revenue, and administers tax laws affecting individuals, businesses, estates, nonprofits, and financial institutions.

With no confirmed commissioner currently in place, questions about decision-making authority have become increasingly significant.

Heated Senate Exchange Focuses on Transparency

The issue gained national attention during questioning from Senator Catherine Cortez Masto.

Throughout the hearing, she repeatedly sought clarification regarding Bessent's exact role within the agency.

When asked directly whether he was serving as acting IRS commissioner, Bessent rejected that characterization.

However, he acknowledged that the responsibilities traditionally associated with the commissioner position ultimately fall under his authority while the role remains unfilled.

The exchange highlighted a legal and administrative distinction that may appear technical but carries important implications regarding oversight, accountability, and public transparency.

For lawmakers, understanding who exercises authority over IRS operations is particularly important given the ongoing legal disputes surrounding taxpayer data leaks and settlement agreements.

The Trump Tax Return Leak Remains a Political Flashpoint

The hearing took place amid continuing scrutiny surrounding a settlement involving President Donald Trump, members of his family, and related business entities.

The controversy stems from one of the largest unauthorized disclosures of taxpayer information in recent U.S. history.

Former IRS contractor Charles Littlejohn admitted to leaking confidential tax information belonging to thousands of taxpayers, including high-profile individuals and business leaders.

The disclosures generated widespread concern about taxpayer privacy protections and the security of sensitive IRS records.

Federal tax law generally treats taxpayer information as among the most protected categories of government-held data. Unauthorized disclosure can result in criminal penalties, civil liability, and significant reputational damage.

The incident prompted lawsuits, investigations, and settlement negotiations involving affected individuals.

Questions Surround a $1.8 Billion Compensation Fund

Adding to the controversy are recent developments involving a proposed $1.8 billion compensation mechanism tied to the Trump settlement.

Justice Department officials recently indicated that a previously planned "anti-weaponization" compensation fund would not move forward as originally envisioned.

However, legal protections connected to the settlement reportedly remain in place.

Those protections include limitations related to audits, enforcement actions, and certain tax matters involving returns filed before the settlement agreement.

The arrangement has raised questions among lawmakers about whether other taxpayers whose information was exposed in the same breach will receive comparable treatment.

Could Other Taxpayers Receive Similar Protections?

One of the central issues raised during the Senate hearing involved fairness and consistency.

Lawmakers noted that approximately 400,000 taxpayers may have been affected by the broader leak of confidential tax information.

The key question posed to Treasury officials was whether those individuals could expect protections similar to those reportedly granted under Trump's settlement.

Critics argue that equal treatment under tax law requires consistent handling of all affected taxpayers regardless of political status, wealth, or public profile.

Supporters of additional review contend that the unique circumstances surrounding the presidential tax return disclosures justify specialized legal arrangements.

When questioned repeatedly about whether other affected taxpayers would receive equivalent protections, Bessent declined to provide a direct answer.

Instead, he emphasized that the Treasury Department is relying on the Justice Department's handling of the litigation and settlement process.

Legal Complexity Continues to Cloud the Issue

The situation is further complicated by ongoing legal proceedings.

Because active litigation remains underway, Treasury officials have indicated they are limited in what they can publicly discuss regarding settlement details, enforcement decisions, and potential remedies available to affected taxpayers.

Legal experts note that settlements involving federal agencies often contain highly specific provisions that may not automatically apply to unrelated parties, even when the underlying circumstances appear similar.

At the same time, lawmakers continue pushing for greater transparency regarding how taxpayer rights are being protected and whether government agencies are applying consistent standards.

Why the Debate Matters Beyond Politics

While the dispute has become politically charged, it also touches on broader issues that affect millions of taxpayers.

Public confidence in the tax system depends heavily on the belief that taxpayer information remains secure and that laws are applied fairly.

Data breaches involving tax records can create risks including:

- Identity theft

- Financial fraud

- Reputational damage

- Unauthorized disclosure of personal information

- Loss of confidence in government institutions

The IRS maintains sensitive records for more than 160 million individual tax filers and millions of businesses each year, making data security one of the agency's most important responsibilities.

Questions surrounding leadership authority, settlement agreements, and taxpayer protections therefore have implications far beyond a single political controversy.

Increased Scrutiny Expected in the Months Ahead

Congressional oversight of the IRS is likely to intensify as lawmakers seek additional details regarding the agency's leadership structure and the implementation of the Trump settlement.

The vacant commissioner position, ongoing litigation, and unresolved questions surrounding taxpayer protections are expected to remain major topics in future hearings.

For now, Bessent has confirmed that while he does not hold the formal title of acting commissioner, he continues to perform many of the duties associated with leading the nation's tax collection agency.

As legal proceedings continue and lawmakers push for more transparency, the debate over IRS leadership, taxpayer privacy, and equal treatment under the law is likely to remain at the center of Washington's fiscal and political discussions.

.webp)

Popular articles

Subscribe to unlock premium content

The Rise of Indoor Vertical Gardening

Esports Tournaments Are Becoming the New Spectator Sport

Minimalism in Motion

The Rise of Indoor Vertical Gardening

Esports Tournaments Are Becoming the New Spectator Sport

The Rise of Indoor Vertical Gardening