Nvidia Signals Fresh Growth Wave as Rubin Platform Begins Customer Rollout

Nvidia Signals Fresh Growth Wave as Rubin Platform Begins Customer Rollout

By

Junia Wells

Last updated:

February 26, 2026

First Published:

February 26, 2026

Photo: Tom's Hardware

Nvidia has reinforced its position at the center of the artificial intelligence boom, projecting another period of rapid expansion as demand for advanced computing infrastructure continues to surge. The company’s latest outlook indicates accelerating momentum, supported by strong orders from cloud providers and the early deployment of its next-generation AI platform.

The forecast highlights how the global race to build AI capacity is still in its early stages, with hyperscalers, enterprises, and model developers continuing to invest heavily in data center hardware.

Revenue Outlook Smashes Expectations

In its latest quarterly report, Nvidia projected revenue of roughly $78 billion for the current period, representing a year-over-year increase of about 77%. The guidance significantly exceeded the consensus estimate of around $72.6 billion and would mark the fastest quarterly growth rate in roughly a year.

The company also delivered strong results for the previous quarter, with revenue climbing 73% annually following 62% growth in the prior period. This marks the 11th consecutive quarter in which revenue expanded by more than 55%, underscoring sustained demand for AI compute capacity.

The data center segment remains the dominant growth engine, now contributing more than 91% of total revenue as customers prioritize high-performance chips and full-stack AI systems.

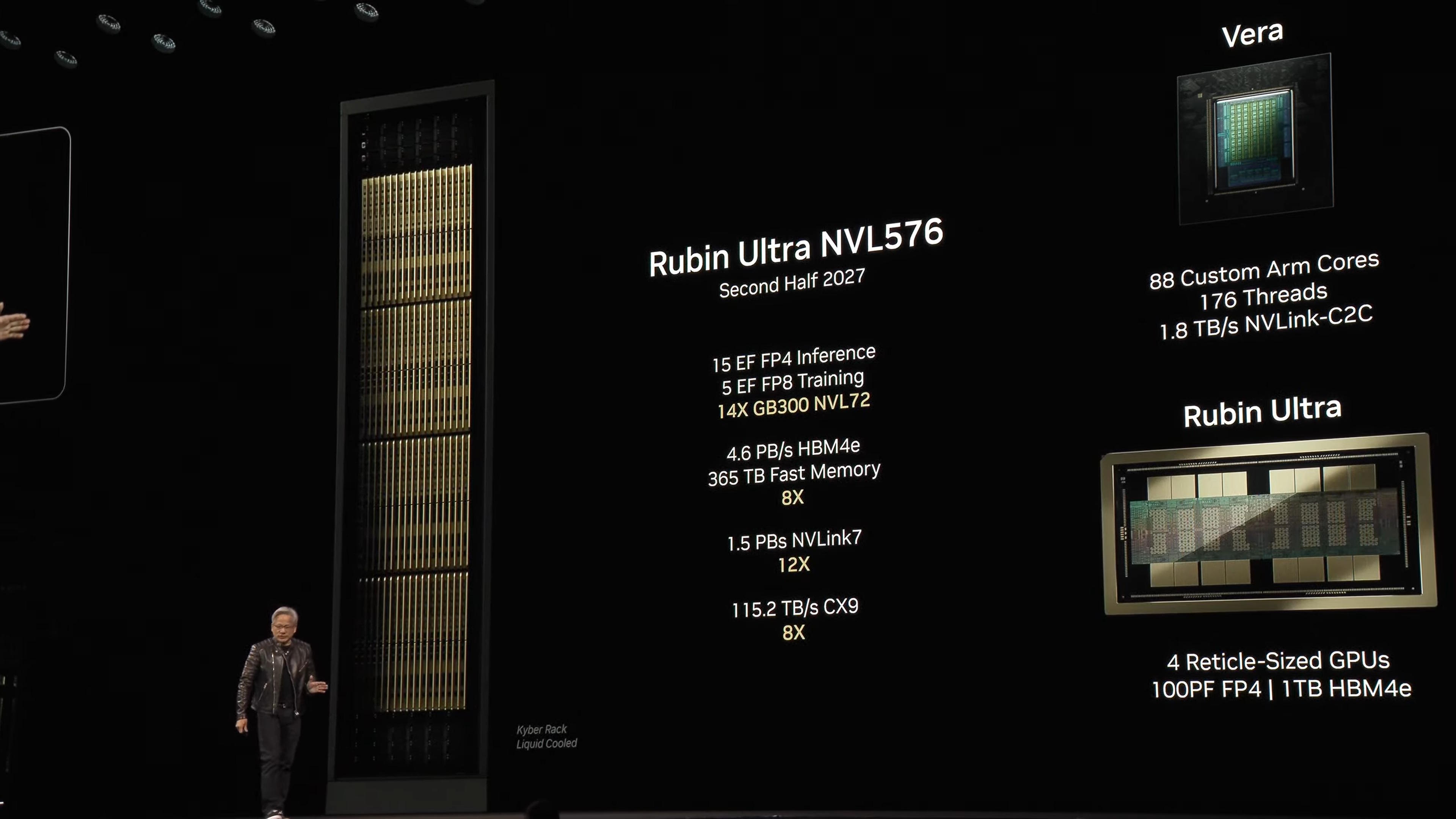

Rubin Platform Marks the Next Phase of AI Infrastructure

A key driver of Nvidia’s optimism is the rollout of its Rubin architecture, the successor to the Grace Blackwell generation. The company confirmed it has begun shipping early samples of the new Vera Rubin rack-scale system to customers, signaling the start of a new upgrade cycle.

The platform integrates 72 next-generation GPUs and is designed to deliver up to ten times better performance per watt compared with previous systems, a metric that is increasingly critical as data center power consumption becomes a limiting factor for AI expansion.

Executives indicated that supply agreements and manufacturing capacity are already in place to support demand through at least 2027, suggesting strong visibility into future orders. Management also said the long-term revenue opportunity tied to the transition from Blackwell to Rubin is likely to exceed earlier projections of a $500 billion market.

Competitive Landscape Intensifies

Despite Nvidia’s dominance, competition in AI hardware is beginning to heat up. Advanced Micro Devices is preparing to launch its Helios rack-scale AI system, with shipments expected to begin next year. Major cloud players are also diversifying supply, including large deployments of AMD GPUs for future data center capacity.

At the same time, some of Nvidia’s largest customers, including Amazon and Google, continue investing in proprietary AI chips to reduce reliance on external suppliers. Nvidia has acknowledged this vertical integration trend as a potential long-term risk, though demand growth currently outweighs competitive pressures.

Market Reaction and Valuation Context

Nvidia’s market capitalization has approached the $5 trillion mark, reflecting investor confidence in its central role in the AI ecosystem. Shares showed limited movement after the earnings release, a sign that expectations were already elevated following the company’s sustained outperformance.

Analysts broadly view the muted reaction as typical for a company operating at such scale, where even strong results must significantly exceed forecasts to drive major stock moves.

Compute Demand Continues to Explode

Chief Executive Jensen Huang emphasized that the rapid expansion of AI workloads is fundamentally reshaping the technology industry. He described a new paradigm in which computing power directly translates into revenue growth for businesses deploying AI applications.

The rise of agentic AI systems, which automate complex workflows and integrate across enterprise software, is driving a new wave of infrastructure spending. Tools from companies such as Anthropic and OpenAI are accelerating adoption by enabling automation across tasks ranging from customer service to software development.

China Remains a Missing Piece

One notable gap in Nvidia’s outlook is the absence of data center revenue from China, where export restrictions and regulatory uncertainty continue to limit sales. Although some shipments of specialized chips have received approval, the company said it is not factoring any China-related revenue into its near-term forecast.

Management estimates that China’s AI infrastructure market could reach roughly $50 billion within a few years, meaning restricted access represents a significant opportunity cost if policy conditions do not change.

Long Term Growth Trajectory

While the near-term outlook remains exceptionally strong, analysts expect growth rates to normalize over time as the market matures. Current projections suggest revenue expansion could slow from more than 60% this year to around 30% the following year, with further deceleration in subsequent periods.

Even with moderating growth, Nvidia’s scale, ecosystem, and software integration position it as a foundational supplier for the AI economy for years to come.

Popular articles

Subscribe to unlock premium content

Estonia The Digital Nomad Paradise

The Rise of Indoor Vertical Gardening

Esports Tournaments Are Becoming the New Spectator Sport

Estonia The Digital Nomad Paradise

The Rise of Indoor Vertical Gardening

Estonia The Digital Nomad Paradise